Gold vs USD: Which Safe Haven Wins in a 2026 Conflict?

When geopolitical tension escalates, traders face a recurring question. In the gold vs USD haven debate, which asset actually protects capital and under what conditions?…

When geopolitical tension escalates, traders face a recurring question. In the gold vs USD haven debate, which asset actually protects capital and under what conditions?

Both assets attract significant inflows during periods of instability. But their mechanics differ. The USD responds to liquidity demand and institutional structure. Gold responds to real yields, inflation expectations, and long-term confidence in fiat systems. Understanding the distinction is what separates reactive trading from structured macro analysis.

This article breaks down how each haven functions, when one outperforms the other, and what macro factors traders should monitor without speculating on any specific event.

Why Traders Look for Safe Havens During Conflict

Conflict introduces systemic uncertainty. Equity markets reprice risk. Credit spreads widen. Commodity supply chains face disruption. In this environment, capital preservation replaces return generation as the primary objective.

This is the core mechanism of a risk-off environment. Traders reduce exposure to assets with high volatility or counterparty risk. Capital is moving out of emerging-market currencies, equities, and high-yield credit. It flows toward assets perceived as stable, liquid, or structurally resilient.

Safe-haven assets serve this function. They are not necessarily high-returning. They are positioned to hold value or gain value when broader markets deteriorate. This capital flight is not random. It follows predictable patterns rooted in macro structure.

The challenge for traders is identifying which haven attracts the most capital in a given scenario. That answer depends on the nature of the conflict, the monetary policy environment, and the current state of real yields and inflation.

Why Gold Is Considered a Safe Haven

Gold has no counterparty risk. A central bank decision cannot devalue it. It carries no default risk. These properties give it a structural role as a store of value during periods when institutional trust erodes.

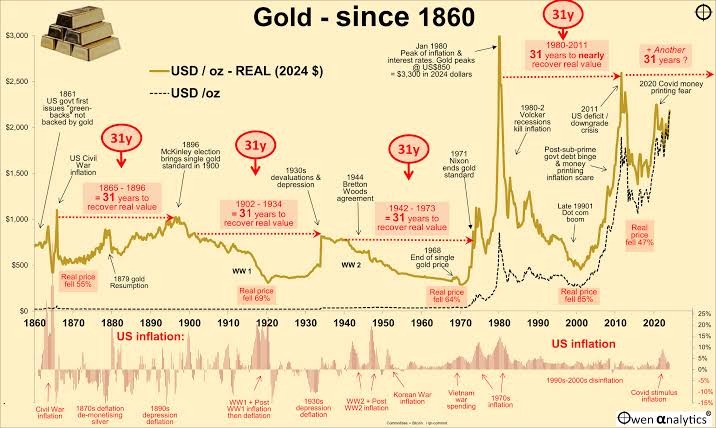

Throughout history, gold has served as a hedge against currency debasement. When governments finance conflict through monetary expansion, the purchasing power of fiat currencies can decline. Gold, priced in those currencies, tends to rise in nominal terms.

This relationship is not mechanical but historically consistent. During the 1970s stagflation period, gold surged as inflation eroded real returns across traditional asset classes. During the 2008 financial crisis, gold rallied as confidence in the banking system collapsed.

Gold is also a hedge against uncertainty itself. When the future paths of inflation, growth, and policy become unclear, investors allocate to assets that retain value across multiple scenarios. Gold fills this role precisely because its supply is constrained and its value is not tied to any single sovereign.

One critical driver of gold pricing is real yields, specifically, US 10-year Treasury yields adjusted for inflation expectations. When real yields fall, the opportunity cost of holding gold declines. Investors are less incentivised to hold yield-bearing assets. Gold becomes more attractive relative to other assets. This inverse relationship between real yields and gold prices is one of the most reliable macro relationships in financial markets.

Why the USD Is the Primary Safe Haven Currency

The US dollar functions as a haven for structural, not sentimental, reasons. It is the world’s dominant global reserve currency. Approximately 60% of global foreign exchange reserves are held in USD. Most international commodity contracts, including oil, are priced in dollars. A significant portion of global debt is denominated in USD.

This structural dominance creates consistent demand. During periods of stress, institutions, corporations, and sovereigns need dollars to meet obligations. This liquidity demand drives inflows into the USD regardless of the underlying cause of the crisis.

In a liquidity crisis, specifically, USD demand spikes. When credit markets seize and risk assets fall sharply, entities scramble for dollars. The 2020 COVID shock demonstrated this clearly. Despite the US being the epicentre of the crisis, the dollar surged in the initial weeks as global liquidity demand overwhelmed any fundamental concerns.

The USD also benefits from the depth of the US Treasury markets. Treasury bonds represent the largest, most liquid sovereign debt market in the world. Investors seeking safety do not just buy dollars; they rotate into US Treasuries, which requires first purchasing USD. This creates a secondary flow mechanism that reinforces dollar strength.

Central bank behaviour compounds this effect. When the Federal Reserve maintains credible inflation-control and interest-rate policy, the USD retains its appeal. When real interest rates are positive, dollar-denominated assets offer both safety and yield, a combination few other currencies can match.

Gold vs USD Safe Haven — Key Differences

The fundamental difference between gold and the USD as safe havens lies in their functions and time horizons.

The USD is primarily a liquidity instrument. In the short term, when markets are stressed and capital needs to move quickly, the dollar absorbs flows because it is the most accessible, most liquid global currency. It is not that traders trust the dollar more; rather, the dollar is structurally embedded in the global financial system.

Gold is primarily a store-of-value instrument. It does not offer yield. It cannot be used directly to settle debts. But it is finite, portable, and sovereign-neutral. When the concern is not short-term liquidity but long-term purchasing power, gold absorbs the relevant flows.

This creates a measurable distinction. In the first hours and days of a crisis, USD strength often dominates. Traders and institutions rush for liquidity. The dollar rises. As the crisis extends, particularly if it involves fiscal expansion, monetary accommodation, or persistent inflation, gold begins to outperform.

The correlation between gold and the USD is typically negative. A stronger dollar makes gold more expensive for non-dollar buyers, compressing demand. A weaker dollar reduces that friction. However, this correlation is not fixed. Both assets can rise simultaneously in severe uncertainty, particularly when neither monetary policy nor fiscal policy offers a credible stabilising response.

Dollar strength also directly affects commodity pricing. Since gold is priced in USD globally, a stronger USD suppresses gold’s price in USD terms, all else equal. This is why traders must always analyse gold alongside real yields and the DXY index, not in isolation.

How Gold and USD Behave During Conflict

Historical patterns from major geopolitical events reveal a consistent sequence of safe-haven behaviour.

In the initial phase of conflict, USD strength tends to dominate. Global institutions, corporations with USD liabilities, and risk-averse capital managers move into dollars and US Treasuries. This initial flow is about liquidity, not valuation. It is mechanical.

Gold’s reaction in the initial phase depends on the interest rate environment. If US real yields are already low or declining, gold responds strongly and quickly. If yields are high or rising, gold’s reaction may be more muted. The opportunity cost of holding a non-yielding asset remains elevated.

As conflict persists, the macro calculus shifts. If the conflict triggers fiscal expansion, increased defence spending, government borrowing, and monetary accommodation, inflation expectations rise. The real yield picture changes. The USD may begin to lose its initial gains as traders price in the medium-term dilutive effects of conflict-driven stimulus. Gold, priced as a real asset, tends to strengthen in this phase.

During the 2003 Iraq War, the USD initially held firm but then weakened over subsequent months as fiscal concerns mounted. Gold extended its rally well beyond the initial period of conflict. During the 2022 Russia-Ukraine conflict, gold spiked sharply on the day of the invasion, while the USD also strengthened, in a dual haven move driven by extreme uncertainty.

Correlation between gold and USD shifts during these periods. Traders who model safe-haven trades as static inverse relationships often get caught. The relationship is conditional, not constant.

When Gold Outperforms the USD

Gold tends to outperform the USD when the dollar’s structural advantages are offset or undermined.

Falling real yields are the clearest trigger. When central banks cut rates or inflation expectations rise faster than nominal yields, real yields decline. Gold’s opportunity cost falls. Capital that would otherwise be invested in yield-bearing USD assets reallocates to gold.

An extended conflict that generates fiscal pressure is historically associated with this dynamic. If a conflict leads to significant government borrowing, bond supply increases. Yields may rise nominally, but if inflation expectations rise faster, real yields still fall. This environment favours gold.

Declining confidence in fiat systems broadly also supports gold over the USD. This occurs when multiple major economies face simultaneous monetary stress, rather than a crisis in a single nation. In scenarios where the dollar faces concerns about debasement alongside other currencies, gold becomes the only true reserve asset free of sovereign risk.

Inflationary conflict environments, where supply chain disruptions, commodity price spikes, and energy market stress compound monetary policy challenges, historically support gold more than the dollar. The 1970s remain the canonical example. Oil shocks, monetary expansion, and geopolitical instability combined to produce a decade-long gold bull market even as the USD faced severe structural challenges.

When the USD Outperforms Gold

The USD outperforms gold when its structural roles as a liquidity provider and a reserve currency are most in demand.

Acute liquidity crises represent the cleanest environment. When credit markets freeze, risk assets collapse suddenly, and institutions face margin calls or funding shortfalls, the demand for dollars overwhelms all other considerations. Capital flees complexity. The dollar is the simplest, deepest, and most accessible haven in that moment.

Rising US interest rates also support USD dominance over gold. When the Federal Reserve tightens policy aggressively, as it did between 2022 and 2023, real yields rise sharply. The opportunity cost of holding gold increases. Yield-bearing USD assets become more attractive by comparison. Capital rotates out of gold and into dollar-denominated fixed income.

Selective geopolitical conflict, where the stress is regional and not broad enough to trigger global inflation concerns, also tends to favour the USD over gold. If conflict does not threaten the global monetary framework, is geographically contained, and does not generate significant commodity supply disruptions, the USD’s liquidity advantage outweighs gold’s store-of-value argument.

Global demand for USD also increases when risk assets globally are underperforming simultaneously. Simultaneous sell-offs across multiple regions push institutional capital into US Treasuries. This Treasury bid reinforces dollar demand. Gold may also rise in this environment, but the magnitude of USD flows typically exceeds gold flows in the short term.

What Traders Should Watch in 2026

Rather than predicting outcomes, traders should monitor specific macro indicators that determine which haven dominates in any given period.

The direction of interest rates is the primary variable. If the Fed is in an easing cycle when a conflict escalates, real yields are likely to fall. That environment is historically favourable for gold. If the Fed is tightening or holding rates high, the USD tends to maintain its relative advantage over gold.

Inflation trends determine the real yield picture. If conflict generates energy price spikes or supply chain disruption that feeds into CPI data, inflation expectations will rise. If equivalent nominal yield increases do not match those rises, real yields fall. Traders should monitor TIPS breakeven rates as a real-time gauge of this dynamic.

Central bank behaviour matters beyond the Fed. If multiple major central banks respond to conflict by expanding balance sheets or cutting rates simultaneously, the dollar’s relative yield advantage narrows. Gold performs better in environments where the entire monetary policy spectrum is accommodative.

Geopolitical escalation pathways determine the duration of haven flows. Short, contained conflicts trigger brief USD spikes followed by mean reversion. Extended conflicts with unclear resolution timelines, commodity supply implications, or fiscal consequences extend the gold bull case. Traders should assess the duration of the conflict and its macro implications, not just the initial headline event.

Dollar index positioning provides a tactical signal. If the DXY is heavily long when conflict begins, the initial USD spike may be limited or short-lived. If positioning is neutral or bearish, there is more room for a dollar rally. The same logic applies to gold futures positioning as reflected in the CFTC Commitment of Traders report.

Key Takeaways

The gold vs USD haven question has no universal answer. Context determines which asset attracts more capital and sustains its gains.

The USD wins in liquidity crises, rising rate environments, and short-term institutional stress. Its dominance is structurally rooted in its status as a reserve currency, Treasury market depth, and the mechanics of global trade finance.

Gold wins when real yields fall, inflation expectations rise, and confidence in fiat monetary policy erodes. Its strength is most durable in extended, fiscally disruptive environments where sovereign monetary credibility comes under pressure.

Both assets can rise simultaneously in extreme uncertainty. The correlation between them is conditional, not fixed. Traders who understand the macro drivers behind each asset, rather than applying static rules, are better positioned to interpret haven flows as they develop.

The interest rate environment, inflation trajectory, and the nature of any geopolitical escalation will determine the gold vs USD safe-haven dynamic in 2026. These are the variables to track. Mechanism, not prediction, is the analytical foundation.

Frequently Asked Questions

Is gold or the USD a better haven?

Neither is universally superior. The USD provides short-term liquidity advantages and is structurally embedded in global finance. Gold provides long-term store-of-value protection, particularly when inflation expectations rise or real yields fall. Which performs better depends on the macro environment at the time of the crisis.

Why does the USD rise during crises?

The USD rises during crises because of structural liquidity demand. A significant portion of global debt, trade contracts, and institutional obligations is denominated in dollars. When financial stress hits, entities need dollars to meet obligations. This demand is mechanical, not a reflection of US economic strength at that moment.

Does gold always go up in a war?

No. Gold’s performance during conflict depends on the interest rate environment, inflation expectations, and the nature of the conflict. If real yields are high when conflict begins, gold’s initial reaction may be muted. If the conflict is brief and contained, gold may quickly give back its initial gains. The strongest gold performance occurs during extended, inflationary conflict environments.

What affects gold prices the most?

Real yields, US Treasury yields adjusted for inflation expectations, are the most reliable macro driver of gold prices. When real yields fall, gold tends to rise, and vice versa. Dollar strength, central bank demand, inflation expectations, and geopolitical uncertainty all contribute, but the real yield relationship is the most analytically consistent.

How do traders use safe-haven assets in their strategies?

Traders use safe-haven assets to hedge risk exposure during periods of uncertainty, to position for capital flows in risk-off environments, and to express macro views on monetary policy divergence. Understanding when each safe haven dominates allows traders to select the right instrument rather than assuming all safe havens behave the same way.

Can gold and the USD both rise at the same time?

Yes. During periods of extreme uncertainty, particularly when neither fiscal nor monetary policy offers a clear stabilising response, both assets can attract simultaneous inflows. The 2022 Russia-Ukraine conflict provided a recent example, with both gold and the USD rising sharply in the early days of the invasion. In these environments, the negative correlation between the two assets temporarily breaks down.